The EU is introducing significant modifications to its VAT legislation, which will become effective on July 1st 2021

We at ArtOn Café are glad to share with you some general news about this VAT legislation. The situation is rapidly evolving, so our information might not always be perfectly updated. Our article is intended as an opportunity to get a rough idea of what is happening and not as legal counseling. ArtOn Café is not responsible for possible actions taken or not taken on the basis of what is presented here.

General context

The modifications to the VAT legislation, which will become effective on July 1st 2021, concern all the business activities addressed to the European public – notably the B2C retailers and the online marketplaces, whether located within or outside the EU (FedEx Express, n.d.-a).

The EU countries are: Austria, Belgium, Bulgaria, Croatia, Republic of Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain and Sweden (European Union, n.d.).

Source: EC-GISCO, © EuroGeographics © UN-FAO for the administrative boundaries (European Union, n.d.)

According to the joint protocol between EU and UK, Northern Ireland will keep the EU VAT tax system for commercial goods. New legislation therefore will be applied only to goods imported into Northern Ireland coming from the rest of the world and not from the EU (FedEx Express, n.d.-a)

The UK and its VAT legislation changes

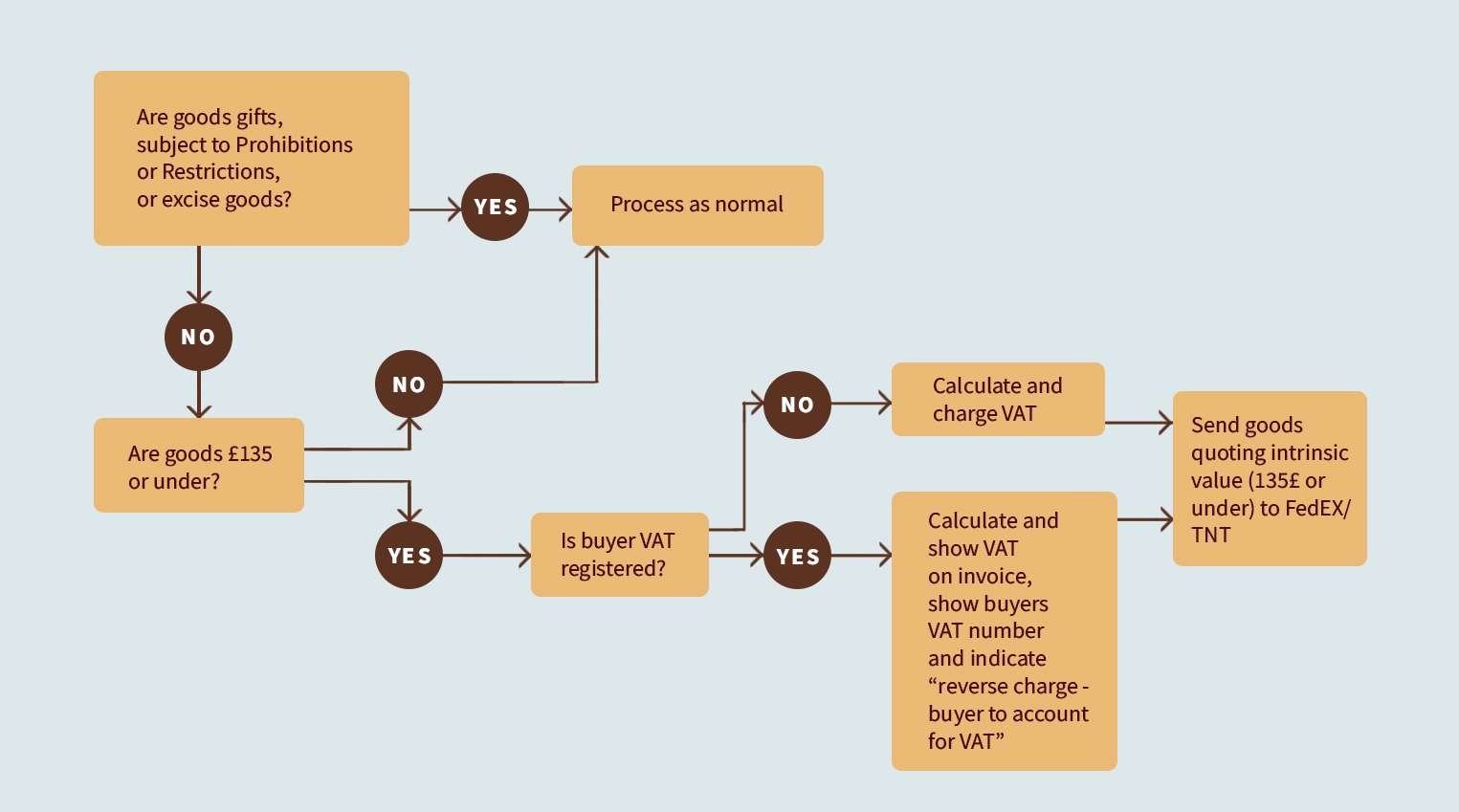

The United Kingdom has already introduced some important changes to its VAT legislation starting from January 2021, after Brexit. Make sure you read about VAT on imports under £135 (FedEx Express, n.d.-b):

Import VAT on goods entering Great Britain (England, Scotland and Wales) with a total value of £135 or less (excluding freight and insurance cost and any other identifiable taxes and charges) has been replaced by supply VAT which is charged by the seller at the time of sale and accounted for by the seller on their regular VAT return. There is no import VAT collected at the time of import. The £135 limit applies to the total value of a consignment that is imported, not the separate value of individual items included in the consignment. If you are an overseas seller and you send goods with a total of £135 or less directly to UK consumers (private individuals and non-VAT registered businesses) you must have a UK VAT registration number. In order to get this, you must establish a UK Government Gateway account – it’s simple to apply and you will only need your email address. You don’t need a UK VAT registration number if you only sell to UK VAT registered businesses. If this is the case, you must quote the buyer’s UK VAT number on the commercial invoice with a note “reverse charge: customer to account for VAT to HMRC”.

Fonte: Picture credits c

For shipments under £135 to Northern Ireland the same process as goods to GB (England, Scotland and Wales) should apply. The difference is that this is not supply VAT but remains import VAT, and is still the responsibility of the overseas seller to account for at time of sale. If NI buyer is VAT registered then the NI buyer’s VAT number should be quoted on the commercial invoice with a note “reverse charge: customer to account for VAT to HMRC”.

If your sales are facilitated by an Online Market Place, they will be responsible for accounting for VAT. In order to charge VAT at the correct rate you must know the specific description of goods you are selling, and their UK VAT rates. You must keep a record of goods you sell and ensure you have full information to apply the correct VAT treatment to them. There are some exclusions from this scheme, and normal import VAT should apply to them: Excise goods, Consumer to Consumer shipments (e.g. gifts), Shipments from Jersey and Guernsey that are covered by the Import VAT Accounting Scheme.

Source – edited: (FedEx Express, n.d.-b)

Take a look at the details concerning imports with a commercial value greater than £135 (FedEx Express, n.d.-b):

Postponed Vat Accounting (PVA) is the scheme introduced by HM Treasury for all UK VAT registered traders and applies to imports with a commercial value greater that £135. PVA enables UK VAT registered importers to account for import VAT on their regular VAT return. There are many benefits to using Postponed VAT Accounting which include: Maintaining uninterrupted cashflow; Reducing administrative burden; Preventing delays to imports.

Removal of the 22€ import VAT exemption

Starting from July 1st 2021, VAT will be charged on all commercial goods imported into the EU, regardless of their value. For consignments with a value up to €150, this can either be charged at the moment of the sale by using the new Import One-Stop Shop (IOSS), or be collected from the end-customer by the customs declarant (FedEx Express, n.d.-a).

EU businesses that make online sale of goods which are located outside the EU to customers within the EU, can opt to use IOSS. If you would like to know more about the Import One Stop Shop (IOSS), please see the European Commission website (FedEx Express, n.d.-a).

Basically, this means that EU businesses selling goods from within the EU member states will not be affected by the removal of the 22€ VAT exemption, while EU businesses selling goods that are imported into the EU will no longer be able to import goods having a value below 22€ free of VAT (FedEx Express, n.d.-a).

Introduction of a One-Stop Shop (OSS)

Businesses that sign up for the One-Stop Shop (OSS) will no longer have to register for VAT in every single EU country they sell in. To sign up for this option, businesses should register on the OSS portal of their EU Member State from April 1st 2021. Along with this, the distance selling VAT threshold regime is being removed by the EU, which means that businesses will have to charge the VAT rate of the customer’s EU country of residence from their first sale, rather than once a certain threshold has been reached. As an exception to the general rule, EU-businesses selling less than €10.000,00 per annum cross-border on B2C goods and services can charge their domestic VAT rate and report the sales in their domestic VAT return. (FedEx Express, n.d.-a).

Finally, the introduction of this new One-Stop Shop system is supposed to reduce complexity and cross-border VAT compliance costs for online sellers. Moreover, it could potentially facilitate greater international trade (FedEx Express, n.d.-a).

Online marketplaces becoming the VAT collector

According to the new EU VAT legislation, certain marketplaces – online platforms facilitating the sales transaction and enabling sellers to sell their goods directly to customers – can become the VAT collector. This means that these marketplaces, rather than the businesses selling through them, will now be responsible for collecting, reporting and remitting the VAT due from the end-customer. The scheme would apply for cross-border or domestic transactions of any value (FedEx Express, n.d.-a).

Basically, businesses and companies which use online marketplaces might be able to de-register for VAT in EU member states, as the marketplace will be both the supplier of the goods and the VAT collector, reducing the administrative burden for EU sellers (FedEx Express, n.d.-a).

Bibliography

European Union. (n.d.). EU Countries. Retrieved April 24, 2021, from About the EU website: https://europa.eu/european-union/about-eu/countries_en

FedEx Express. (n.d.-a). Changes to EU VAT rules. Retrieved April 24, 2021, from https://www.fedex.com/en-it/eu-vat-changes.html#:~:text=From July 1%2C 2021%2C VAT,the EU%2C regardless of value.&text=EU businesses that make online,can opt to use IOSS.

FedEx Express. (n.d.-b). Changes to UK VAT rules. Retrieved from https://www.fedex.com/content/dam/fedex/eu-europe/brexit/vat/FedEx_Brexit_VAT_Changes_EN.pdf

Picture credits a: Rawpixel.com. Retrieved April 27, 2021, from https://www.shutterstock.com/it/image-photo/value-added-tax-vat-finance-taxation-247492816

Picture credits b: Constantin Stanciu. Retrieved April 27, 2021, from https://www.shutterstock.com/it/image-photo/closeup-on-notebook-over-vintage-desk-1109925662

Picture credits b: Constantin Stanciu. Retrieved April 27, 2021, from https://www.shutterstock.com/it/image-photo/closeup-on-notebook-over-vintage-desk-1109925662